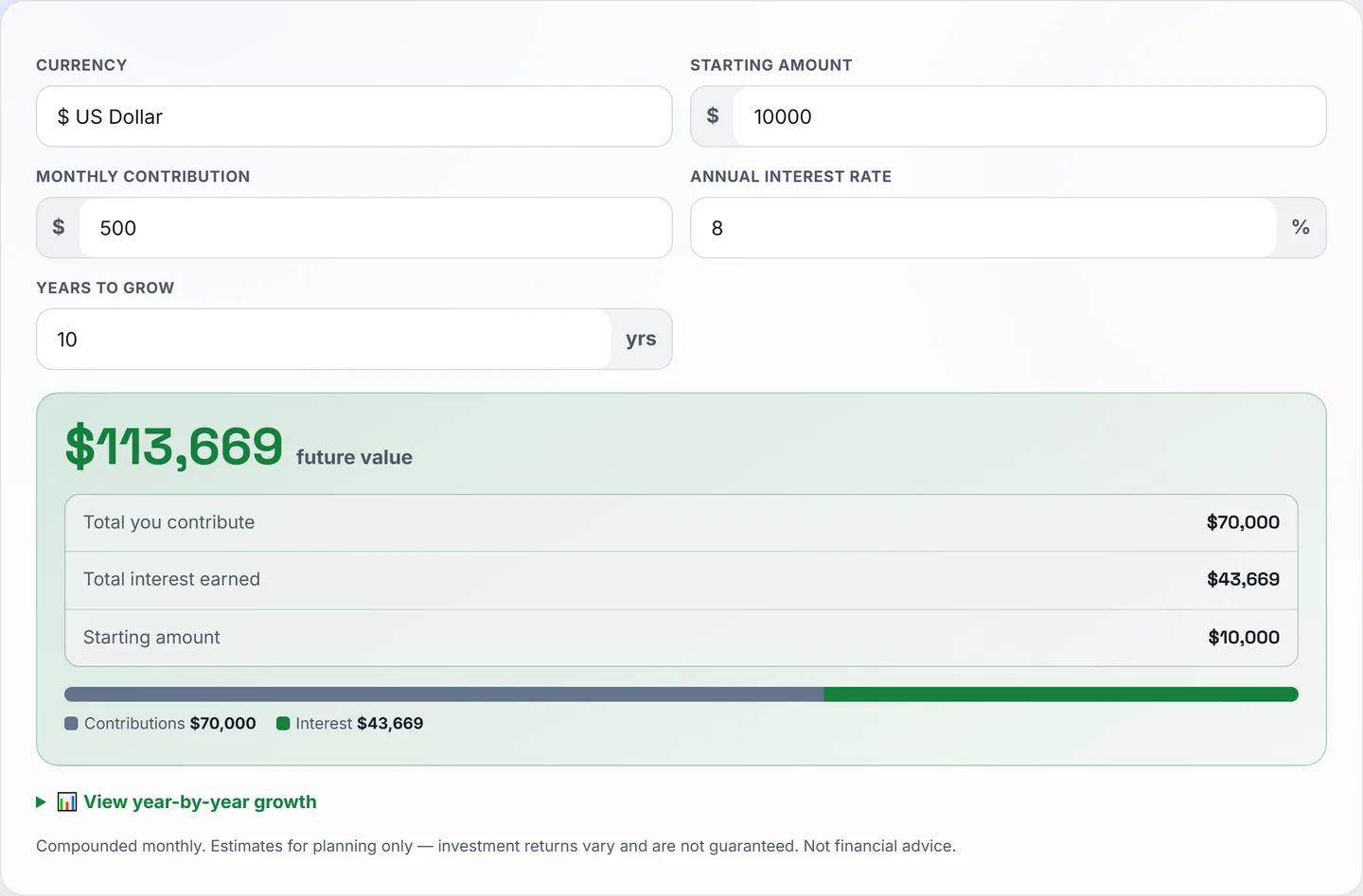

Compound interest is the reason small, boring, regular amounts of money turn into surprisingly large ones — and also the reason credit card debt gets out of hand so fast. The idea fits in one sentence: each period, you earn interest on your interest. What that sentence hides is how violently the effect accelerates with time, so this guide walks through the actual numbers.

Simple vs compound — the same 100,000

Put 100,000 somewhere earning 8% per year for 10 years:

| Year | Simple interest | Compound (annual) |

|---|---|---|

| 1 | 108,000 | 108,000 |

| 3 | 124,000 | 125,971 |

| 5 | 140,000 | 146,933 |

| 10 | 180,000 | 215,892 |

Simple interest pays 8,000 every year forever — a straight line. Compound interest pays 8,000 in year one, then 8,640, then 9,331… because each year's interest joins the balance and starts earning itself. After a decade the gap is already 35,892, and it keeps widening — the curve bends upward while the straight line just plods.

The formula

- P — starting amount · r — annual rate as a decimal · n — compounding periods per year · t — years

Worked: 100,000 at 8% compounded monthly for 10 years → A = 100,000 × (1 + 0.08/12)120 = 221,964. Monthly compounding beats annual (215,892) by about 6,000 — nice, but notice it's a small bonus compared with what the rate and the years did. Frequency is the seasoning, not the meal.

The Rule of 72

For quick mental math, divide 72 by the annual return to get the approximate doubling time:

| Annual return | Money doubles in ≈ |

|---|---|

| 4% | 18 years |

| 8% | 9 years |

| 12% | 6 years |

| 24% (credit card, working against you) | 3 years |

That last row is the one to remember: an unpaid card balance at 24% doubles in roughly three years. Compounding is neutral — it accelerates whatever balance it's attached to, including the ones you owe.

Why starting early beats investing more

The most famous compounding example, run through our calculator at 10% annual return, monthly compounding, 5,000 per month:

| Early starter | Late starter | |

|---|---|---|

| Invests | Age 25–35, then stops | Age 35–60, never stops |

| Total put in | 600,000 | 1,500,000 |

| Value at 60 | ≈ 12.35 million | ≈ 6.63 million |

The early starter invests less than half the money and ends with nearly double. The ten extra years of compounding on the early contributions outweigh 15 years of additional deposits. There is no trick here — it's the exponent in the formula doing exactly what exponents do.

Where you meet compounding in real life

- Savings accounts and fixed deposits — usually quoted with annual or monthly compounding; the quoted APY already includes it.

- Index funds and pensions — returns compound because gains stay invested; this is where the early-starter math above plays out.

- Credit cards — interest compounds on unpaid balances, typically daily or monthly. The Rule of 72 row above is why minimum payments barely move the balance. Our Debt Payoff Calculator shows the escape route.

- Loans quoted "per month" — a 2% monthly rate is not 24% a year; compounded, it's 26.8%. Always convert before comparing.

Three mistakes to avoid

- Interrupting it. Withdrawing gains restarts the curve at the flat end. The dramatic growth in every table above lives in the final third of the timeline.

- Comparing rates with different compounding. 7.9% compounded monthly beats 8% compounded annually. Compare APY (the effective annual yield), not the headline number.

- Forgetting inflation. Real growth = return minus inflation. At 10% return with 6% inflation, your real compounding rate is roughly 4% — still powerful, but plan with honest numbers.

Educational content, not investment advice — returns in real markets vary year to year, and past performance never guarantees the future.