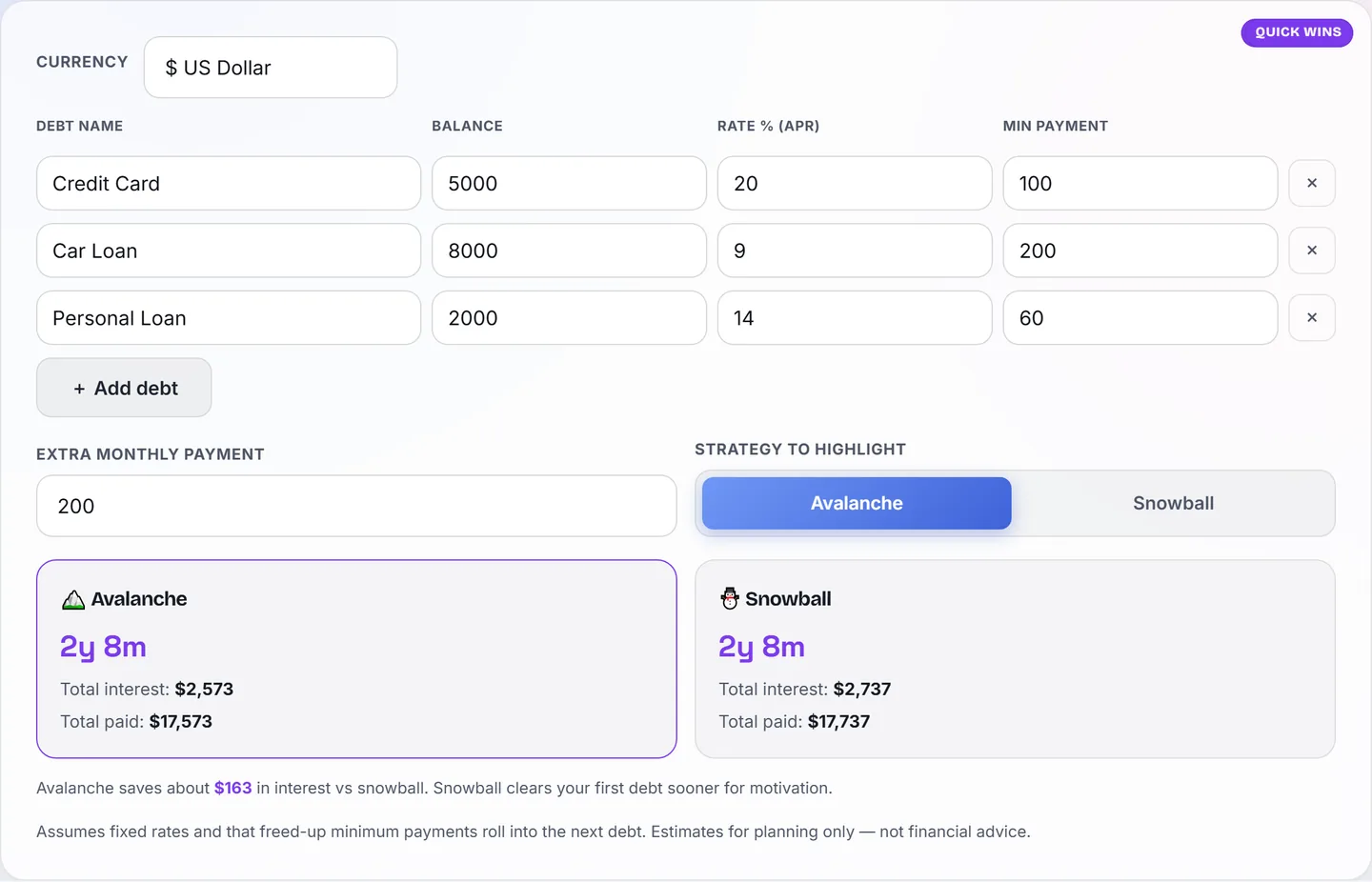

When you owe money in several places — a credit card, a personal loan, a car loan — the order you attack them in genuinely changes what you pay. There are two famous strategies, and the internet argues about them endlessly. Instead of arguing, we simulated both, month by month, on the same set of debts, using the same simulation engine that powers our Debt Payoff Calculator. The results are below, to the unit.

The two strategies in one minute

- Snowball: pay minimums on everything, throw every spare unit at the smallest balance. When it dies, roll its whole payment into the next smallest. Built for motivation — quick visible wins.

- Avalanche: pay minimums on everything, throw every spare unit at the highest interest rate. Built for math — the least total interest, guaranteed.

The test case

Three debts, and a total budget of 22,000 a month (minimums add up to 17,000, so there is 5,000 extra to aim):

| Debt | Balance | Interest rate | Minimum payment |

|---|---|---|---|

| Credit card | 250,000 | 24% | 7,500 |

| Personal loan | 80,000 | 12% | 2,500 |

| Car loan | 300,000 | 9% | 7,000 |

Note the setup: the smallest debt (the personal loan) is not the most expensive one. That's the situation where the two strategies genuinely part ways — and it's extremely common in real life.

The results

| Snowball | Avalanche | |

|---|---|---|

| Payoff order | Personal → Card → Car | Card → Personal → Car |

| First debt cleared | Month 12 | Month 26 |

| Debt-free | Month 36 | Month 36 |

| Total interest paid | 154,882 | 140,856 |

Three honest observations from the simulation:

- Avalanche saved 14,026. Aiming at the 24% card first stops the most expensive meter earliest. That saving is real money and it always lands on avalanche's side.

- Both finished in the same month. Total payoff time is set by how much you pay per month, not the order. The order decides the interest bill and the shape of the journey.

- Snowball's first win came 14 months sooner. One debt gone inside a year versus waiting over two years for the first "paid off" moment. If that early win is what keeps you paying the extra 5,000 instead of drifting back to minimums, it can be worth more than 14,026.

So which should you pick?

Our honest reading of the numbers:

- Pick avalanche if you're numbers-driven and the rate gap between your debts is big (a 24% card next to a 9% loan, like above). The saving is too large to ignore.

- Pick snowball if you've tried and abandoned payoff plans before. The method that survives is the method that works — an abandoned avalanche saves nothing.

- Hybrid: a popular compromise is to snowball one small debt first for the quick win, then switch to avalanche for everything else. In our example that costs only a few thousand more than pure avalanche and still delivers the month-12 morale boost.

Making either method work

- Never skip minimums on the debts you're not targeting — late fees and penalty rates wipe out months of progress.

- Roll payments forward. When a debt dies, its entire payment joins the attack on the next one. That acceleration is the whole point of both methods.

- Stop adding new debt while paying off — a card that keeps getting used is a bucket with a hole in it.

- Recheck after rate changes. If a promotional 0% period ends or a floating rate moves, the avalanche order can change.

This guide is educational, not personal financial advice. If your situation involves collections, penalty interest or hardship, a licensed debt counsellor will give you options a calculator can't.