An EMI — equated monthly instalment — is the fixed amount you pay every month on a loan until it is cleared. The bank quotes it in seconds, and most borrowers accept it as a mystery number. It isn't. The EMI comes from one standard formula, and understanding it changes how you negotiate: you'll see exactly what a longer tenure really costs, why the first year of payments barely touches your balance, and how lenders use "flat rates" to disguise expensive loans.

The formula

- P — the principal (amount borrowed)

- r — the monthly interest rate = annual rate ÷ 12 ÷ 100

- n — number of monthly instalments (years × 12)

This is the standard reducing-balance amortization formula used by banks worldwide for home, car and personal loans. It is built so that every instalment covers that month's interest on whatever you still owe, plus a slice of the principal — sized precisely so the balance hits zero on the last payment.

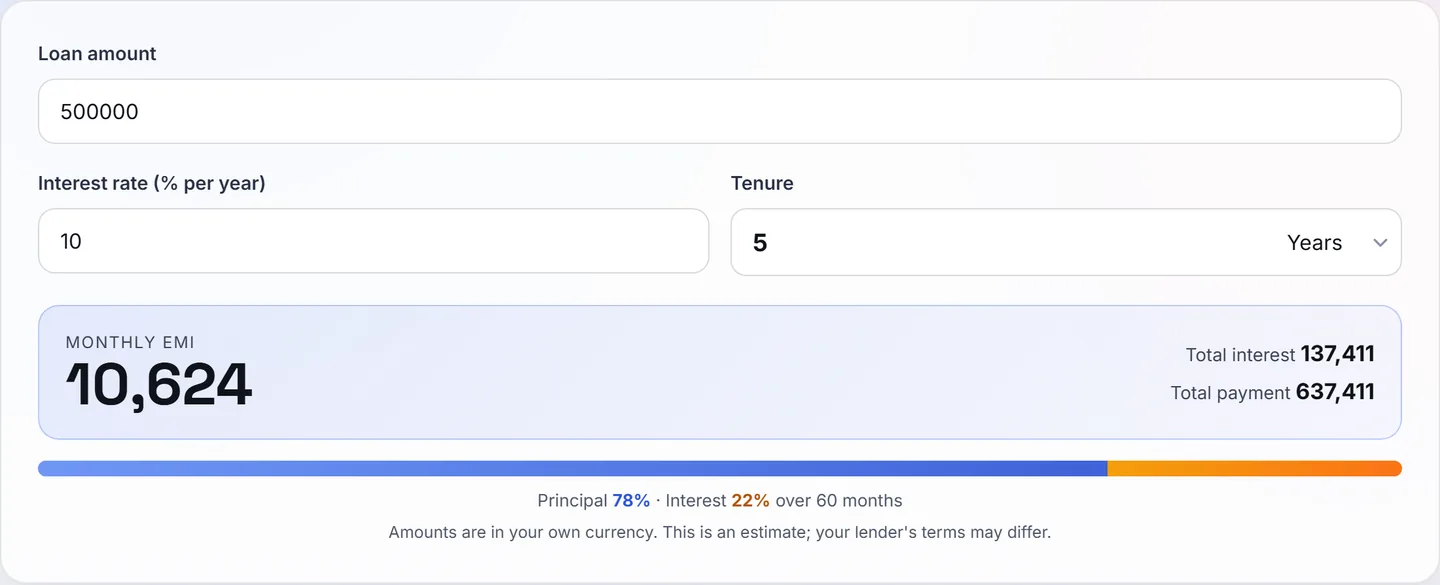

Worked example: 500,000 at 10% for 5 years

Let's borrow 500,000 (any currency — the math is identical) at 10% per year for 5 years:

- Monthly rate: r = 10 ÷ 12 ÷ 100 = 0.008333

- Instalments: n = 5 × 12 = 60

- Growth factor: (1 + 0.008333)60 = 1.6453

- EMI: 500,000 × 0.008333 × 1.6453 ÷ (1.6453 − 1) = 6,855 ÷ 0.6453 ≈ 10,624

So the loan costs 10,624 a month. Over 60 months you pay 637,411 in total — the 500,000 you borrowed plus 137,411 in interest. Here is the same calculation done live in our calculator:

Where each instalment goes (amortization)

Interest is always charged on the outstanding balance. At the start the balance is huge, so interest eats most of the instalment:

| Month | Interest part | Principal part | Balance after |

|---|---|---|---|

| 1 | 4,167 | 6,457 | 493,543 |

| 2 | 4,113 | 6,511 | 487,032 |

| 3 | 4,059 | 6,565 | 480,466 |

| 30 | 2,494 | 8,130 | 291,181 |

| 60 (last) | 88 | 10,536 | 0 |

Notice the flip: month 1 is 39% interest; the final month is under 1%. This is why prepaying early in a loan saves so much more than prepaying late — an extra payment in year one kills interest on that money for the entire remaining term.

Tenure: the lever that cuts both ways

| Tenure | EMI | Total interest |

|---|---|---|

| 3 years | 16,134 | 80,808 |

| 5 years | 10,624 | 137,411 |

| 7 years | 8,301 | 197,254 |

| 10 years | 6,608 | 292,904 |

Stretching from 5 to 10 years drops the EMI by 4,016 a month — and adds roughly 155,000 of interest. The honest way to choose: pick the shortest tenure whose EMI you can genuinely afford, generally keeping total EMIs under 35–40% of monthly income.

The flat-rate trap

Some lenders — especially for car and personal loans — quote a "flat rate": interest computed on the original amount for the whole term, ignoring the fact that you're paying it down. A 6% flat rate on our 5-year example charges 500,000 × 6% × 5 = 150,000 interest — slightly more than the 10% reducing-balance loan above. As a rule of thumb, a flat rate is roughly equivalent to a reducing rate of 1.8–1.9× the number. Always ask for the reducing-balance APR before comparing.

Related calculators for specific loans

- Mortgage Calculator — home loans, with amortization schedule and extra-payment modelling.

- Auto Loan Calculator — car loans, including down payment and trade-in.

- Debt Payoff Calculator — juggling several debts? See the payoff order that costs least.

This guide is for education, not financial advice. Lenders add fees, insurance and rounding rules of their own — confirm the final schedule with your bank before signing.