Zakat is one of the five pillars of Islam: an annual 2.5% of qualifying wealth, given to those entitled to receive it. The obligation is simple to state and surprisingly fiddly to compute the first time — which assets count, what nisab means, whose gold price, which debts deduct. This guide walks the whole calculation once, with numbers, so your own takes five minutes. We built our Zakat Calculator around exactly this method.

Step 1 — Know the nisab

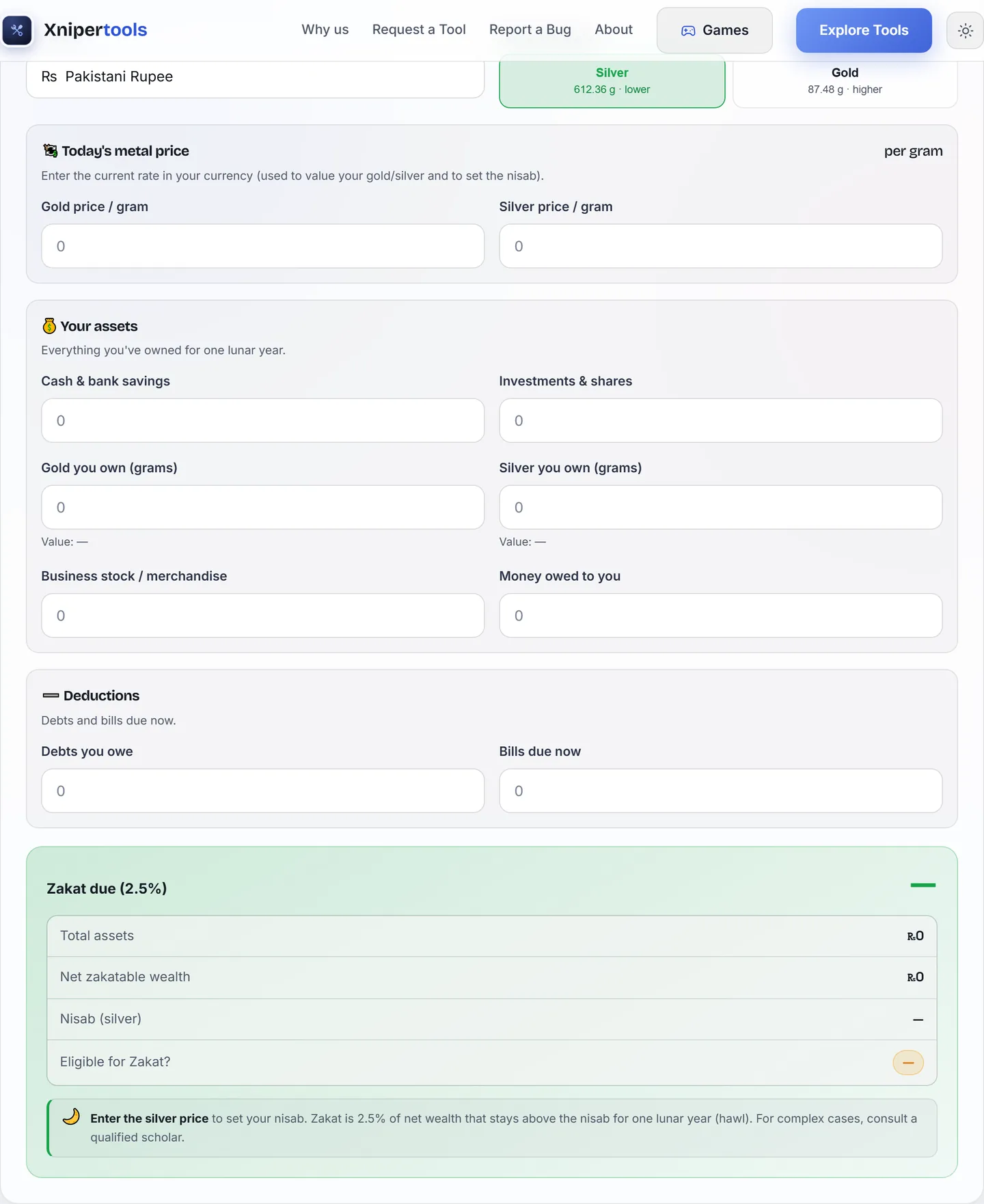

Nisab is the wealth threshold below which zakat is not due. It's defined in precious metal, valued at today's market price:

| Standard | Amount | How to value it |

|---|---|---|

| Gold nisab | 87.48 g (7.5 tola) | 87.48 × today's gold price per gram |

| Silver nisab | 612.36 g (52.5 tola) | 612.36 × today's silver price per gram |

Because silver is far cheaper, the silver nisab is a much lower threshold — using it means zakat becomes due on more modest savings. Many scholars call that the safer and more charitable opinion; the gold standard is also valid and widely followed. If your zakatable wealth stays at or above nisab for one full lunar year (hawl ≈ 354 days), zakat is due on the anniversary.

Step 2 — List what counts

| Zakatable ✔ | Not zakatable ✖ |

|---|---|

| Cash — in hand, bank accounts, wallets | Your home you live in |

| Gold and silver (jewellery included in most opinions) | Car(s) for personal use |

| Business stock / inventory at sale value | Furniture, clothes, phone, tools of your trade |

| Money reliably owed to you | Property you live in or use (not for trade) |

| Shares/funds held for trading; savings plans | — |

Step 3 — Deduct immediate debts

Debts that are currently due — this month's bills, instalments payable now, money you owe that will be collected — are generally deducted from the total before comparing with nisab. Long-term loans (like a multi-year mortgage) are treated differently across schools of thought: some deduct only the current year's instalments, some none. When it materially changes your number, ask your local scholar.

Step 4 — The worked example

| Item | Amount |

|---|---|

| Cash in bank + wallet | 800,000 |

| Gold (valued at today's price) | 150,000 |

| Committee/savings fund | 250,000 |

| Total zakatable assets | 1,200,000 |

| Minus: debts currently due | −200,000 |

| Net zakatable wealth | 1,000,000 |

Check against nisab: suppose today's silver nisab works out to about 250,000 in local currency. Net wealth of 1,000,000 is above it, and it has been held a full lunar year — so zakat is due:

Zakat = 1,000,000 × 2.5% = 25,000

That's the entire calculation. The 2.5% rate applies to money, gold, silver and trade goods; agricultural produce and livestock have their own separate rates and rules not covered here.

Practical tips from doing this yearly

- Fix your zakat date. Many people use a Ramadan date for the reward multiplier — any date works if you keep it consistent year to year.

- Value metals on the day. Gold and silver prices move; use the price on your zakat date, not the purchase price.

- Fluctuating balances: the common practical approach is to check that wealth stayed above nisab at the start and end of the lunar year — dips in between don't restart the year in most opinions.

- Keep last year's sheet. Your asset list barely changes; next year becomes a 10-minute update instead of a fresh audit.

This guide explains the widely followed general method for educational purposes. Detailed rulings differ between schools of thought and personal situations — for anything unclear or high-stakes, consult a qualified scholar.